Highlights

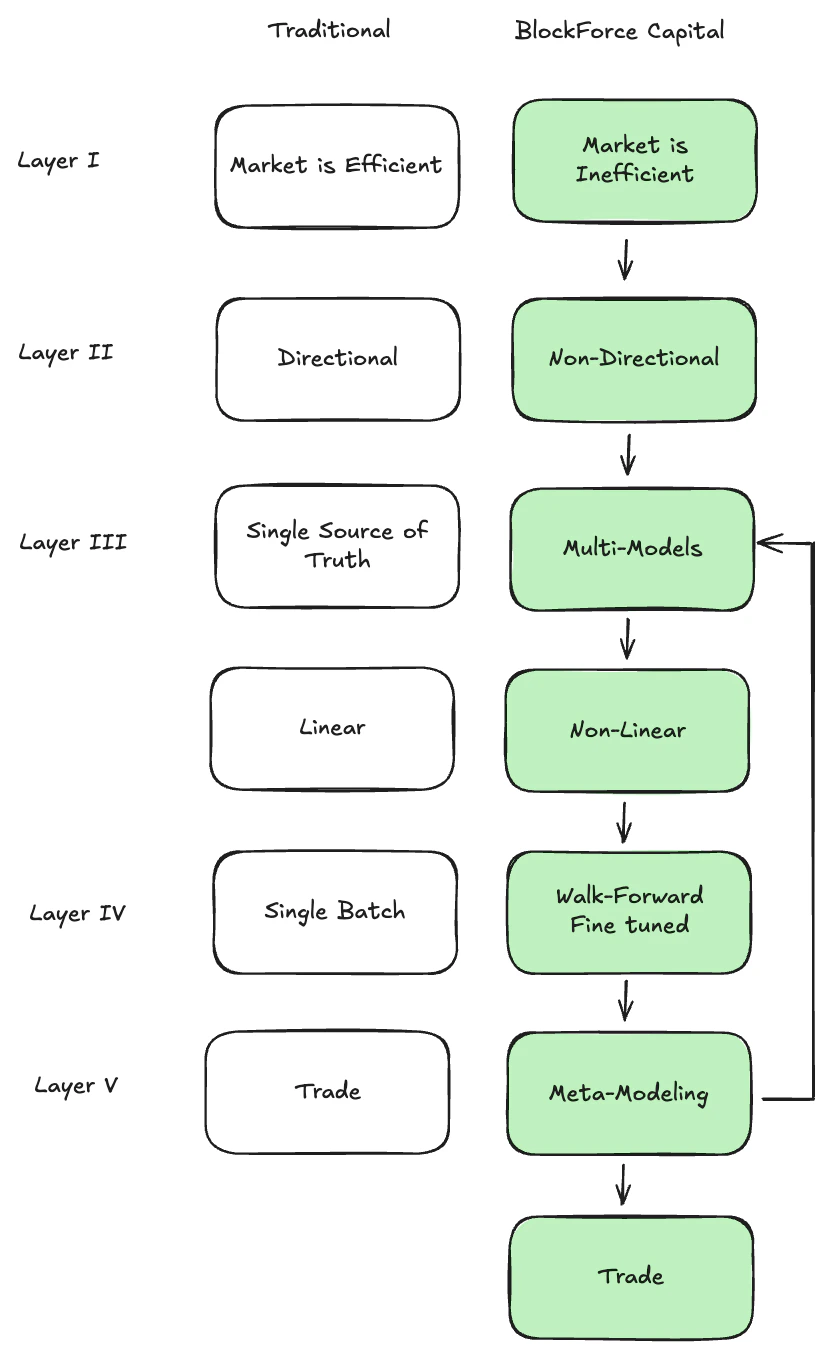

Statistical arbitrage operates on identifying pricing inefficiencies (or discrepancies), where long or short positions are taken in opposite directions when the prices of an asset or group of assets deviate from their expected relationships or equilibrium.

- Market-Neutral Portfolio Construction : Designing portfolios with factor-neutral exposures, ensuring that systematic risks are eliminated. This involves optimizing weights so that the portfolio’s aggregate sensitivity to predefined factors (e.g., market beta) sums to zero.

- Non-Parametric and Non-Linear Approaches : Dependency modeling that avoids assumptions of linear relationships or reliance on correlation coefficients. This enables detection of strong non-linear associations, including rare and extreme market events that traditional methods might overlook.

- Speed Optimization : The pipeline leverages vectorized operations to maximize computational efficiency. Code is compiled wherever possible, reducing execution time for large-scale datasets and allowing rapid backtesting and real-time analytics.

- Code Modularity : Code is modular and designed with reusable components, making it easy to maintain, extend, and adapt for different use cases. Each module is purpose-built for a specific function, promoting clarity and reducing redundancy across the codebase. This ensures scalability and facilitates team collaboration on larger projects.

Strategies

Examples of how to apply the methodologies and tools described in this repository can be found in theexamples/notebooks directory. These Jupyter notebooks demonstrate various quantitative analysis techniques, including model implementation, custom indicators, signal generation, and backtesting, providing practical insights and hands-on guidance for users.

Disclaimer and Limitations

- Backtest Overfitting and Selection Bias: Academics and practitioners often conduct thousands of backtests to find promising investment strategies, but the best-performing result is typically presented as if it were a single trial. This selection bias leads to many false discoveries in finance, explaining why many funds fail to meet expectations.

- Backtesting is Validation, Not Research: In the scientific method, testing aims to refute hypotheses, but in finance, backtesting is often misused to create trading rules. This creates a circular process: researchers backtest thousands of rules, propose the best-performing one as a hypothesis, and use the same backtest as evidence to support it.

- Develop Theories, Not Trading Rules: Backtesting alone is insufficient for reliable conclusions. Researchers should develop theories independently of backtesting, using methods like feature importance analysis to avoid overfitting. A robust theory explains phenomena through clear cause-effect mechanisms, which must be validated through unbiased backtesting and evidence against the theory’s implications.

- Changing Market Conditions: While academics have focused on type I (false positive) and type II errors (false negative) for investment strategy development, they have failed to analyze changing market conditions. Traders are interested less in knowing the statistical significance of their strategies, than in knowing whether their strategy will work in the future. Whether it will work in the future is dependent on the durability of market conditions which existed while developing it. for example, factor investing strategies often determine the cheapness or richness of a security as a function of their exposure to a few fundamental factors, which are reported infrequently. These models do not adjust quickly to changing market conditions.

- Avoid All-Regime, Favor Regime-Specific Strategies: Academics and practitioners often seek investment strategies that perform well in all market regimes, such as risk premia or risk parity. However, true “all-regime” strategies are rare due to market adaptability and investor learning. Even if they exist, they likely represent a small subset of strategies effective in specific regimes. More information could be found in Tactical investment algorithms.

- Variance is Evenly Distributed Across Components: Factor investing relies on representing variables through principal components, ideally fewer than the original variables. This reduces model dimensions by capturing most of the variance with a limited number of components. However, if variance is evenly distributed across components, the reduction fails, resulting in as many components as initial variables.

- Distribution Shifts and Extreme Events: Investment strategies often assume that the underlying market conditions remain stable over time. However, real-world markets are dynamic, with frequent distribution shifts caused by changes in economic regimes, technological advancements, regulatory environments, or investor behavior. These shifts can render previously successful strategies ineffective or even counterproductive. Addressing distribution shifts requires adaptive models capable of identifying and responding to structural changes in the market, as well as stress testing strategies across a wide range of possible scenarios.