systematica, including statistical arbitrage models, range-based strategies, meta-learning approaches, and factor models.

These models form the core quantitative strategies that generate trading signals from market data.

For signal processing and conversion to trading decisions, see Signal Processing.

For portfolio simulation and backtesting, research workflows and hyperparameter optimization, see Portfolio Management.

Model Architecture Overview

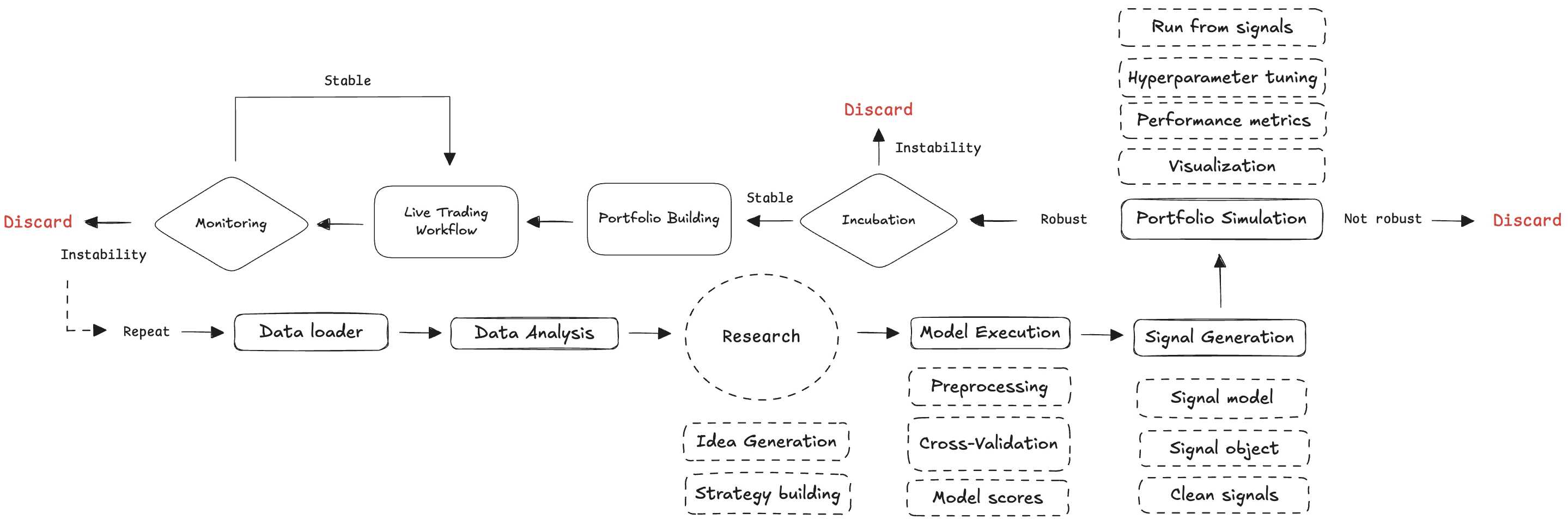

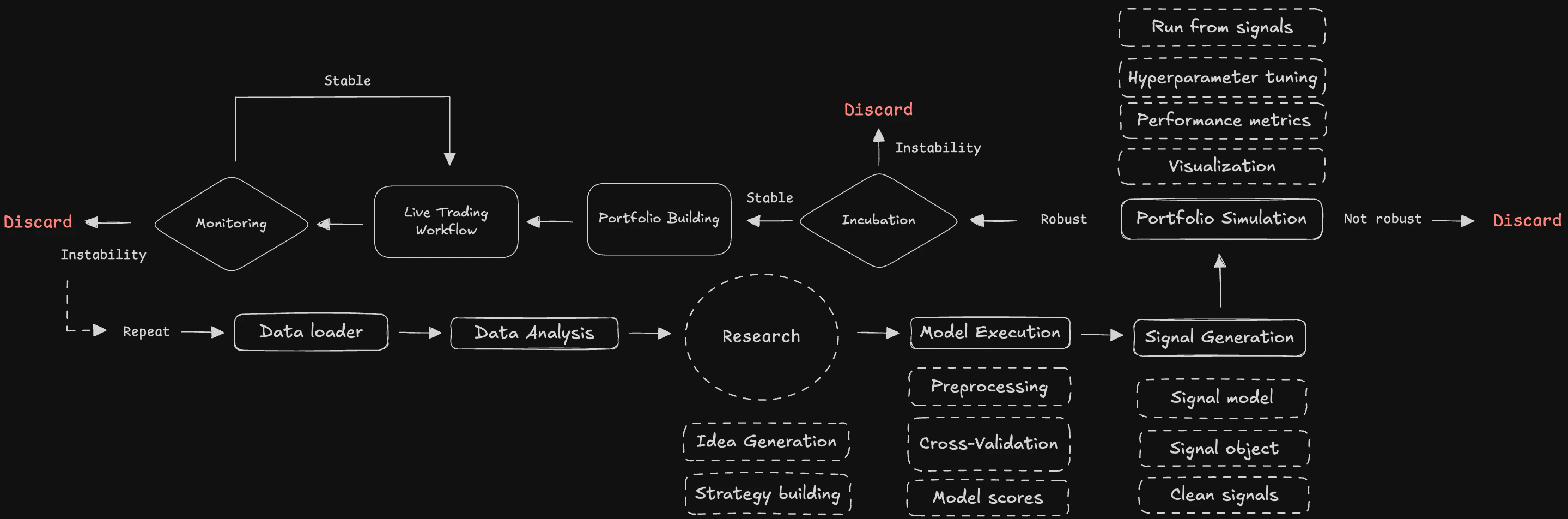

Systematica implements a hierarchical model architecture built around theBaseStatArb base class, which provides standardized interfaces for model execution, signal generation, and portfolio simulation.

Sub-modules

- systematica.api.models.arbitrage_index

- systematica.api.models.meta_model

- systematica.api.models.momentum

- systematica.api.models.ou_process

- systematica.api.models.range_breakout

- systematica.api.models.spread

- systematica.api.models.volatility

- systematica.api.models.volume_profile